Navigating 2026 COBRA Premium Assistance: Your Comprehensive Guide to Extended Health Coverage

In an ever-evolving landscape of healthcare policy, understanding your options for continued health coverage is paramount. For many, the Consolidated Omnibus Budget Reconciliation Act (COBRA) serves as a critical safety net, allowing individuals and their families to maintain group health benefits after certain qualifying events. As we look towards 2026, the prospect of COBRA Premium Assistance becomes a focal point for those navigating job transitions, reductions in hours, or other life changes that might otherwise disrupt their healthcare. This comprehensive guide delves into the nuances of the COBRA Premium Assistance 2026 program, offering practical solutions and strategic insights to ensure you and your loved ones remain covered.

The importance of uninterrupted health coverage cannot be overstated. Unexpected medical emergencies, ongoing treatments, or even routine check-ups can quickly become financially debilitating without proper insurance. COBRA was enacted to bridge this gap, providing a temporary continuation of health coverage. However, the cost of COBRA premiums can often be a significant barrier. This is where premium assistance programs, like the one potentially relevant for 2026, play a vital role, making COBRA coverage more accessible and affordable during challenging times.

This article aims to demystify the COBRA Premium Assistance 2026, breaking down complex regulations into understandable terms. We will explore who is eligible, what benefits are covered, the duration of assistance, and the steps you need to take to enroll and maintain your coverage. Our goal is to equip you with the knowledge and resources necessary to make informed decisions about your healthcare future.

Understanding COBRA: The Foundation of Continued Coverage

Before we can fully appreciate the value of COBRA Premium Assistance 2026, it’s essential to grasp the fundamentals of COBRA itself. COBRA is a federal law that allows employees and their families to continue group health benefits provided by their employer for a limited period after certain events, such as job loss, reduction in hours, death, divorce, or other life changes. This continuation of coverage is generally at the individual’s expense, meaning you pay the full premium plus a small administrative fee, which can be substantial.

Who is Covered by COBRA?

COBRA applies to group health plans maintained by private-sector employers with 20 or more employees, and to state and local governments. It does not apply to federal government plans or to church plans. Additionally, some states have their own “mini-COBRA” laws that provide similar continuation coverage for employees of smaller employers (typically fewer than 20 employees) not covered by federal COBRA.

Qualifying Events for COBRA

To be eligible for COBRA, a “qualifying event” must occur. These events typically include:

- Termination of employment (for reasons other than gross misconduct)

- Reduction in hours of employment

- Death of the covered employee

- Divorce or legal separation from the covered employee

- A covered employee becoming entitled to Medicare

- A child ceasing to be a dependent under the plan rules

Each qualifying event has specific implications for who can elect COBRA coverage and for how long.

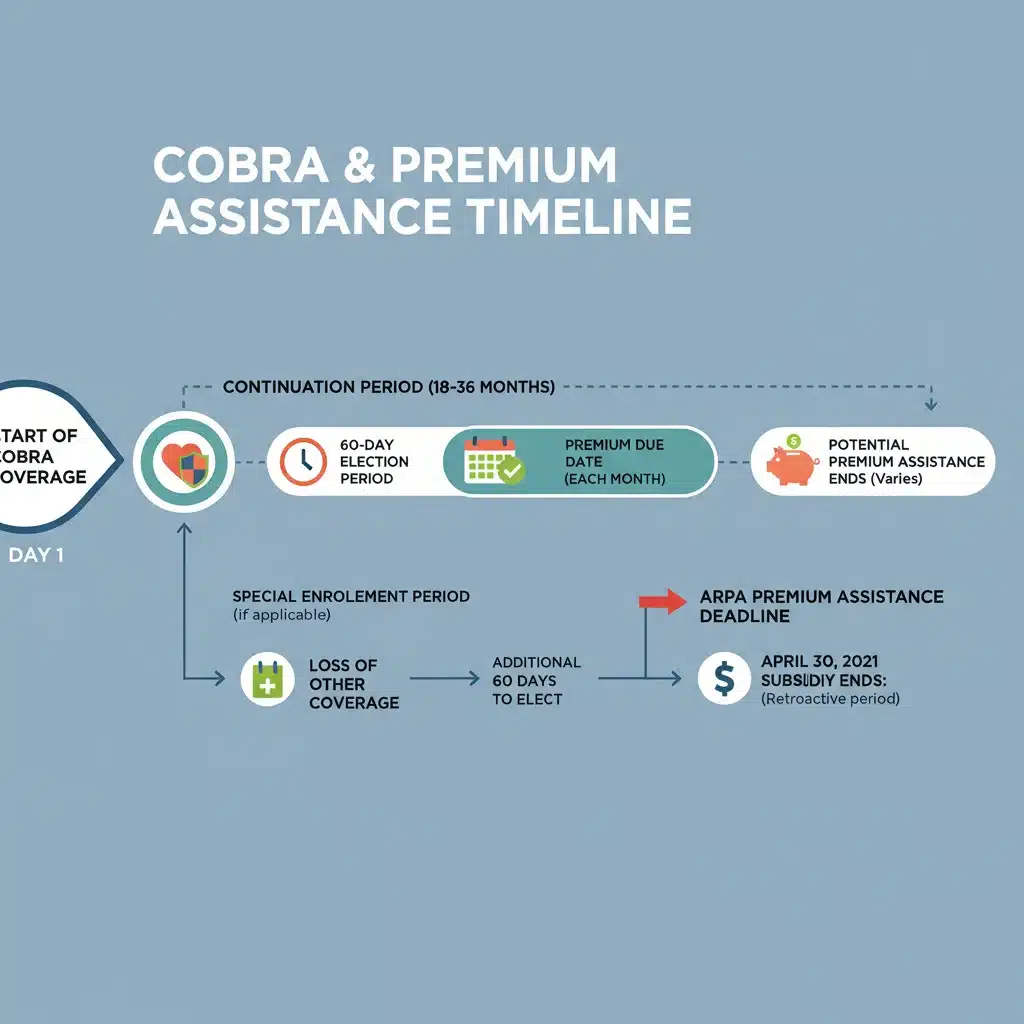

Duration of COBRA Coverage

The standard maximum period for COBRA coverage is 18 months for qualifying events such as employment termination or reduction in hours. However, in certain circumstances, this period can be extended:

- 29 months: If a qualified beneficiary is determined by the Social Security Administration (SSA) to be disabled at any time during the first 60 days of COBRA coverage, or if the qualified beneficiary is determined disabled before the qualifying event and the disability continues through the first 60 days of COBRA.

- 36 months: For other qualifying events, such as death of the covered employee, divorce, or a child ceasing to be a dependent.

It’s crucial to understand these durations, as they directly impact how long any premium assistance might apply.

The Significance of COBRA Premium Assistance

While COBRA provides a vital lifeline, its cost can be prohibitive. The individual is responsible for paying the entire premium, which can be as much as 102% of the cost to the plan (the employer’s share plus the employee’s share, plus a 2% administrative fee). This is where premium assistance programs step in, offering financial relief to make COBRA coverage more attainable.

Historically, there have been periods where federal legislation has provided COBRA premium subsidies, most notably during economic downturns or public health crises. These subsidies significantly reduce or even eliminate the out-of-pocket cost for eligible individuals, making continued health coverage a realistic option during periods of transition.

Why is COBRA Premium Assistance 2026 Important?

As we approach 2026, discussions around potential economic shifts and healthcare affordability continue. A COBRA Premium Assistance 2026 program, if enacted, would be instrumental in supporting individuals and families facing job loss or other qualifying events. It would alleviate the financial burden of high COBRA premiums, allowing people to maintain continuity of care without incurring significant debt or foregoing essential medical services. This continuity is not just about physical health; it also contributes to mental well-being and financial stability during uncertain times.

Eligibility for COBRA Premium Assistance 2026 (Anticipated Criteria)

While the specific details of any COBRA Premium Assistance 2026 program would depend on future legislation, we can draw insights from past programs to anticipate potential eligibility criteria. Typically, these programs target individuals who have experienced involuntary termination of employment or a reduction in hours, making them eligible for COBRA.

Key Eligibility Factors to Consider:

- Qualifying Event: Most premium assistance programs have historically focused on specific qualifying events, primarily involuntary termination of employment. It’s crucial to distinguish between voluntary resignation and involuntary termination, as the latter is almost always a prerequisite for assistance.

- COBRA Election: You must elect COBRA coverage to be eligible for premium assistance. If you let your COBRA election period expire, you generally cannot retroactively receive assistance.

- No Other Group Health Coverage: Typically, individuals are not eligible for premium assistance if they are eligible for other group health plan coverage (e.g., through a new employer or a spouse’s employer) or Medicare. The assistance is designed for those who would otherwise be uninsured or face significant financial hardship to maintain coverage.

- Income Limitations (Potential): While not always present in past assistance programs, some legislative proposals or future iterations could include income thresholds to target assistance to those most in need. This is a factor to monitor as any new legislation emerges.

How to Determine Your Eligibility

The first step in determining your eligibility for COBRA Premium Assistance 2026 (should it become available) is to understand your COBRA rights. Your employer is legally required to provide you with a COBRA election notice after a qualifying event. This notice will explain your rights, the cost of coverage, and the election period. Pay close attention to this document, as it forms the basis of your COBRA journey.

If a premium assistance program is enacted, your employer or plan administrator will likely be responsible for notifying you of your potential eligibility and providing the necessary forms and instructions. It is critical to keep your contact information updated with your former employer to ensure you receive these important communications.

Benefits and Duration of COBRA Premium Assistance 2026

The core benefit of COBRA Premium Assistance 2026 would be the significant reduction or elimination of COBRA premiums. This financial relief can be transformative, allowing individuals to continue their existing health plan without the burden of high monthly costs. This means maintaining access to their current doctors, specialists, and treatment plans, ensuring continuity of care.

What Does “Assistance” Typically Cover?

Past premium assistance programs have covered a substantial portion, if not all, of the COBRA premium. For example, some programs have provided a 100% subsidy, meaning eligible individuals paid nothing for their COBRA coverage during the assistance period. Other programs might cover a percentage, such as 65% or 75%, still offering considerable savings.

It’s important to note that the assistance typically applies only to the premium for the health coverage itself. Any additional costs, such as deductibles, co-payments, or co-insurance, would still be the responsibility of the qualified beneficiary, unless specifically stated otherwise in the legislation.

Anticipated Duration of Assistance

The duration of COBRA Premium Assistance 2026 would be a critical detail of any new legislation. Historically, assistance periods have varied, ranging from a few months to over a year. For example, some programs offered assistance for up to 18 months, aligning with the standard COBRA coverage period for job loss or reduced hours.

It’s crucial to understand that the premium assistance period is often distinct from the maximum COBRA coverage period. For instance, you might be eligible for 18 months of COBRA coverage, but only 9 months of premium assistance. After the assistance period ends, you would then be responsible for the full COBRA premium for the remainder of your eligibility.

Careful planning and budgeting would be essential to manage the transition if the assistance period is shorter than your total COBRA eligibility. This is a key area where proactive engagement with your plan administrator and financial planning can make a significant difference.

The Application and Enrollment Process for COBRA Premium Assistance 2026

Navigating the application and enrollment process for COBRA, let alone potential premium assistance, can seem daunting. However, understanding the steps involved can streamline the experience and ensure you don’t miss crucial deadlines.

Step-by-Step Guide (Anticipated):

- Receive Your COBRA Election Notice: After a qualifying event, your employer or plan administrator must send you a COBRA election notice. This notice typically arrives within 14 days after the plan administrator receives notice of the qualifying event. Read this document carefully.

- Elect COBRA Coverage: You generally have 60 days from the date you receive your COBRA election notice (or the date your coverage would otherwise end, whichever is later) to elect COBRA. This is a critical deadline. Even if you anticipate premium assistance, you must first elect COBRA.

- Receive Premium Assistance Notification: If a COBRA Premium Assistance 2026 program is enacted, your plan administrator will likely send you a separate notice regarding your eligibility for the subsidy and how to apply. This notice will include specific forms and instructions.

- Complete and Submit Assistance Forms: Fill out all required forms accurately and completely. This may include certifications that you meet the eligibility criteria (e.g., involuntary termination, no other group coverage).

- Monitor Your Coverage: Once approved, ensure your coverage is active and that premiums are being paid (either by the assistance program or by you, if applicable, after the assistance period). Keep records of all communications and submissions.

Important Deadlines and Retroactive Coverage

Deadlines are paramount in COBRA. Missing an election deadline can mean forfeiting your right to COBRA coverage entirely. Similarly, any deadlines associated with a premium assistance program will be critical. In some past programs, individuals who had already elected and paid for COBRA coverage before the assistance program began were eligible for reimbursement of premiums paid during the assistance period. This is known as retroactive coverage and would be a key detail to look for in any COBRA Premium Assistance 2026 legislation.

Alternatives to COBRA and Premium Assistance

While COBRA Premium Assistance 2026 could offer significant relief, it’s not the only option for continued health coverage. It’s always wise to explore all available avenues to ensure you choose the best fit for your needs and budget.

The Health Insurance Marketplace (Affordable Care Act – ACA)

The Health Insurance Marketplace, established under the Affordable Care Act (ACA), is a robust alternative to COBRA. A qualifying event, such as job loss resulting in loss of employer-sponsored coverage, triggers a Special Enrollment Period (SEP) on the Marketplace. This allows you to enroll in a new plan outside of the annual open enrollment period.

- Subsidies: Unlike COBRA, which requires you to pay the full premium (unless assistance is available), the Marketplace offers premium tax credits and cost-sharing reductions based on income. Many individuals find plans on the Marketplace to be more affordable than COBRA, even without premium assistance.

- Plan Options: The Marketplace typically offers a wider range of plans from different insurers, allowing you to choose a plan that best meets your specific healthcare needs and budget.

Medicaid and CHIP

For individuals and families with lower incomes, Medicaid and the Children’s Health Insurance Program (CHIP) can provide comprehensive, low-cost or free health coverage. Eligibility for these programs is based on income and family size, and applications can be submitted at any time.

Spouse’s Employer-Sponsored Plan

If you have a spouse, losing your job-based health coverage is a qualifying event that allows you to enroll in their employer-sponsored plan, often without waiting for an open enrollment period. This can sometimes be the most cost-effective and straightforward option.

Short-Term Health Insurance

Short-term health insurance plans offer temporary coverage, typically for up to a year. While they are often less expensive than COBRA or Marketplace plans, they also offer fewer benefits and do not have to comply with ACA requirements, meaning they may not cover pre-existing conditions or essential health benefits. They are generally not recommended as a long-term solution but can serve as a bridge in very specific circumstances.

Comparison: COBRA vs. Marketplace

When considering COBRA versus the Marketplace, especially in the context of potential COBRA Premium Assistance 2026, weigh the following:

- Continuity of Care: COBRA allows you to keep your existing plan, which is ideal if you want to continue seeing your current doctors and have ongoing treatments.

- Cost: Without premium assistance, COBRA is often more expensive. With assistance, it could be very affordable. Marketplace plans, with subsidies, can also be highly cost-effective.

- Benefits: COBRA maintains your employer’s plan benefits. Marketplace plans vary, so you’d need to compare coverage carefully.

- Flexibility: The Marketplace offers more choice in plans. COBRA offers continuity but no new plan selection.

Strategic Planning for Your Health Coverage in 2026

Proactive planning is key to navigating healthcare transitions effectively. As 2026 approaches, and with it the potential for COBRA Premium Assistance 2026, consider these strategic steps:

Stay Informed

Keep abreast of legislative developments regarding COBRA and potential premium assistance. Follow reputable news sources, government agency updates (e.g., Department of Labor, IRS), and healthcare advocacy groups. This information will be critical for understanding the specifics of any enacted program.

Review Your Employer’s Health Plan Documents

Familiarize yourself with the details of your current employer-sponsored health plan. Understand what it covers, its costs, and how COBRA would apply. This knowledge will be invaluable when comparing COBRA to other options.

Understand Your COBRA Rights and Election Period

Know the timeline for electing COBRA. Even if you’re hoping for premium assistance, you must first secure your COBRA election option within the designated timeframe. Don’t let this crucial window close.

Evaluate All Your Options

Don’t put all your eggs in the COBRA basket, even with potential premium assistance. Always compare COBRA (with and without assistance) against Marketplace plans (with potential subsidies), your spouse’s plan, Medicaid, and CHIP. Use the Marketplace website (HealthCare.gov) to explore plan options and estimate subsidies.

Budget for Potential Costs

Even with premium assistance, there might be out-of-pocket costs like deductibles, co-pays, and co-insurance. If the assistance is not 100%, you’ll also have a portion of the premium to cover. Budgeting for these expenses is vital for financial stability.

Seek Professional Advice

If you find the options complex, consider consulting with a benefits administrator, a financial advisor, or a healthcare navigator. These professionals can offer personalized guidance based on your unique situation.

The Future of COBRA Premium Assistance

The landscape of healthcare policy is dynamic, and the specific provisions of COBRA Premium Assistance 2026 will depend on legislative action. However, the precedent set by previous assistance programs highlights a recognition of the financial challenges associated with maintaining health coverage during periods of unemployment or reduced hours.

As advocacy groups continue to push for greater healthcare access and affordability, it is plausible that future legislation will consider mechanisms to support individuals in transitional phases. Whether this takes the form of direct premium subsidies, enhanced tax credits for Marketplace plans, or a combination of approaches, the goal remains to prevent gaps in coverage and protect individuals from catastrophic healthcare costs.

Staying engaged with these policy discussions and understanding the potential impact on your personal healthcare planning is an ongoing responsibility. The ability to adapt and make informed choices will be your greatest asset in navigating the complexities of health insurance.

Conclusion: Securing Your Health Coverage in 2026 and Beyond

The prospect of COBRA Premium Assistance 2026 offers a beacon of hope for many who may face disruptions in their employer-sponsored health coverage. By understanding the foundational principles of COBRA, anticipating the potential eligibility criteria and benefits of premium assistance, and exploring all available alternatives, you can make empowered decisions about your healthcare future.

Remember that continuous health coverage is not merely a financial safeguard; it is a cornerstone of overall well-being. It ensures access to necessary medical care, promotes preventive health, and provides peace of mind during uncertain times. As you plan for 2026, prioritize staying informed, carefully evaluating your options, and acting decisively within critical deadlines.

Your health is your most valuable asset. By taking proactive steps today, you can ensure that you and your family maintain the comprehensive health coverage you deserve, regardless of life’s unexpected turns. The journey through healthcare options can be intricate, but with the right information and strategic approach, you can navigate it successfully, ensuring your access to quality care for up to 18 months or even longer, through programs like COBRA Premium Assistance 2026.