Maximize Savings: Your 2026 Tax-Loss Harvesting Guide

Maximize Savings: Your 2026 Tax-Loss Harvesting Guide

As we navigate the ever-evolving landscape of personal finance, smart strategies are paramount to optimizing your wealth. One such powerful, yet often underutilized, tactic is tax-loss harvesting 2026. This guide will provide you with a comprehensive, step-by-step approach to understanding and implementing this strategy, helping you reduce your capital gains and potentially lower your overall tax bill by up to $3,000 annually.

The year 2026 brings its own set of economic nuances and market conditions that savvy investors should consider. By strategically selling investments that have decreased in value, you can offset capital gains from other profitable investments. Beyond that, you can even deduct a portion of any remaining losses against your ordinary income. This technique, while seemingly simple, requires careful execution and a thorough understanding of IRS rules to avoid pitfalls.

What is Tax-Loss Harvesting?

At its core, tax-loss harvesting is the practice of selling securities at a loss to offset a capital gains tax liability. When you sell an investment for more than you paid for it, you realize a capital gain. Conversely, selling an investment for less than you paid means you realize a capital loss. The U.S. tax code allows investors to use these capital losses to reduce their taxable capital gains.

The primary benefit of tax-loss harvesting 2026 is its ability to reduce your tax burden. For every dollar of capital gains you have, you can offset it with a dollar of capital losses. If your capital losses exceed your capital gains, you can then use up to $3,000 of those net capital losses to reduce your ordinary income (such as salary, wages, or interest income) in a given tax year. Any remaining losses can be carried forward indefinitely to offset future capital gains or ordinary income.

This strategy is particularly beneficial during periods of market volatility or downturns, as it allows investors to turn temporary market dips into tangible tax savings. However, it’s not just for bear markets. Even in bull markets, individual securities can underperform, providing opportunities for harvesting losses.

Why is Tax-Loss Harvesting Relevant for 2026?

While the fundamental principles of tax-loss harvesting remain constant, market conditions, economic forecasts, and potential legislative changes can influence its effectiveness and the specific strategies employed. As we look towards 2026, understanding the broader financial environment is key. Interest rate policies, inflation trends, and global economic stability all play a role in market performance, creating both opportunities for growth and potential for losses that can be harvested.

Furthermore, staying informed about any proposed or enacted tax legislation is crucial. While the core rules for capital gains and losses tend to be stable, minor adjustments can sometimes occur that might affect how losses are treated or how capital gains rates are applied. Regular review of tax laws ensures you are always optimizing your strategy for tax-loss harvesting 2026.

The Mechanics of Tax-Loss Harvesting: A Step-by-Step Guide

Implementing a successful tax-loss harvesting strategy involves several key steps. Adhering to these steps ensures that you comply with IRS regulations and maximize your tax benefits.

Step 1: Identify Underperforming Investments

The first step is to review your investment portfolio for positions that are currently trading below their purchase price. These are your potential candidates for harvesting losses. It’s important to look at both short-term and long-term investments.

- Short-term losses: These result from selling an investment you’ve held for one year or less. They first offset short-term capital gains, which are typically taxed at your ordinary income tax rate.

- Long-term losses: These result from selling an investment you’ve held for more than one year. They first offset long-term capital gains, which are generally taxed at lower preferential rates.

Ideally, you want to use short-term losses to offset short-term gains, and long-term losses to offset long-term gains. If you have an excess of one type of loss, it can then be used to offset the other type of gain before being applied to ordinary income.

Step 2: Calculate Your Realized and Unrealized Gains/Losses

Before you make any moves, you need a clear picture of your current capital gains and losses. Your brokerage statements will typically provide this information. Sum up all your realized capital gains (from investments you’ve already sold for a profit) and realized capital losses (from investments you’ve already sold at a loss) for the current tax year.

Then, look at your unrealized losses – these are investments you still hold that are currently trading below your cost basis. These are the assets you’ll consider selling to realize the loss. This calculation is vital for effective tax-loss harvesting 2026.

Step 3: Strategically Sell Losing Positions

Once you’ve identified your underperforming assets, you can sell them to realize the capital loss. The timing of this sale is crucial, especially as you approach the end of the tax year. Most investors aim to harvest losses before December 31st to ensure they count for the current tax year.

When selling, consider the amount of loss you need. If you have a significant amount of capital gains, you might need to sell more losing positions. If your goal is to deduct against ordinary income, remember the $3,000 annual limit.

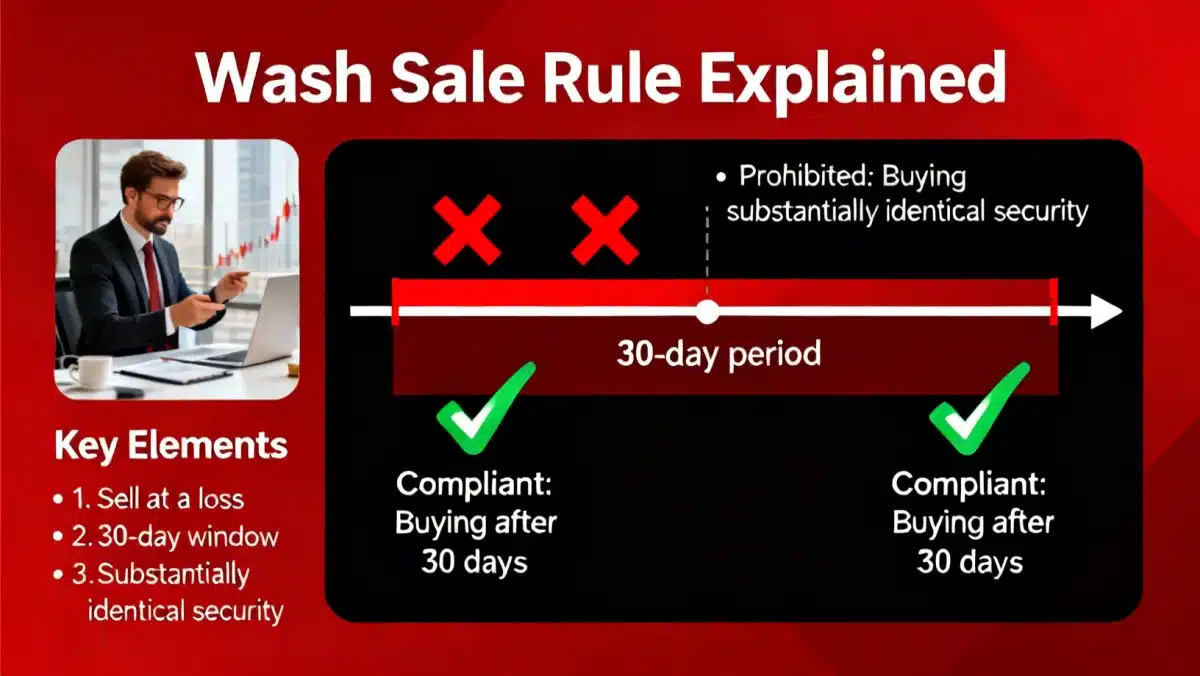

Step 4: Understand and Avoid the Wash Sale Rule

This is arguably the most critical and often misunderstood aspect of tax-loss harvesting. The IRS’s wash sale rule prevents investors from claiming a loss on a security if they buy a “substantially identical” security within 30 days before or after the sale date. This 61-day window (30 days before, the day of the sale, and 30 days after) is designed to prevent investors from selling a security just to claim a loss and then immediately repurchasing it to maintain their market position.

What constitutes a “substantially identical” security? This can be tricky. Generally, it refers to shares of the same company or very similar exchange-traded funds (ETFs) that track the same index. For example, if you sell shares of Apple (AAPL) at a loss, you cannot buy more Apple shares within the 30-day window. However, you could potentially buy shares of a different company in the same sector or an ETF that holds Apple but also many other stocks, provided it’s not considered substantially identical.

To avoid a wash sale, you have a few options:

- Wait the 31 days before repurchasing the same security.

- Buy a similar, but not substantially identical, security. For instance, if you sell an S&P 500 index ETF, you could buy a total stock market ETF or a different S&P 500 ETF from a different provider with a slightly different composition or methodology.

- Do not repurchase any security for the 61-day window.

Failing to adhere to the wash sale rule means your realized loss will be disallowed for tax purposes, and the disallowed loss is added to the cost basis of the newly acquired shares, deferring the loss until those new shares are sold.

Step 5: Document Everything

Maintain meticulous records of all your investment transactions, especially those related to tax-loss harvesting 2026. This includes purchase dates, sale dates, cost basis, sale proceeds, and the resulting capital gains or losses. Your brokerage firm will typically provide a Form 1099-B, which reports your sales proceeds, but you are responsible for tracking your cost basis and wash sale adjustments.

Accurate documentation is crucial for correctly filling out Schedule D (Capital Gains and Losses) and Form 8949 (Sales and Other Dispositions of Capital Assets) when you file your taxes.

Advanced Strategies for Tax-Loss Harvesting

Beyond the basic steps, there are several advanced considerations that can enhance your tax-loss harvesting 2026 efforts.

Consider Your Overall Tax Situation

Your personal tax bracket and overall income level should influence your harvesting strategy. If you are in a high-income bracket, the value of offsetting ordinary income with the $3,000 net capital loss deduction is more significant. Conversely, if you have very low income, you might prefer to carry forward losses to a year when you anticipate higher income or significant capital gains.

Tax-Loss Harvesting in Retirement Accounts (Generally Not Applicable)

It’s important to note that tax-loss harvesting typically applies only to taxable brokerage accounts. You cannot harvest losses in tax-advantaged accounts like 401(k)s or IRAs, as gains and losses within these accounts are not taxed until withdrawal (in the case of traditional accounts) or are tax-free (in the case of Roth accounts). The IRS rules for capital gains and losses do not apply to transactions within these accounts.

Harvesting Throughout the Year vs. Year-End

While many investors focus on year-end harvesting, opportunities can arise throughout the year, especially during market corrections or individual stock downturns. Harvesting losses periodically can be more effective than waiting until December, as it allows you to react to market conditions and potentially avoid a rush of transactions closer to the deadline.

Automated tax-loss harvesting services offered by robo-advisors or certain brokerage platforms can also help in this regard, continuously monitoring your portfolio for harvesting opportunities.

Rebalancing Your Portfolio

Tax-loss harvesting can be integrated with your portfolio rebalancing strategy. When you sell a losing position, you can use the proceeds to purchase a different asset that helps you maintain your desired asset allocation. This allows you to harvest losses without significantly altering your long-term investment strategy, provided you avoid the wash sale rule.

Understanding the Long-Term Impact of Basis Adjustments

When you sell an investment at a loss and then purchase a ‘substantially identical’ security within the wash sale window, the disallowed loss is added to the cost basis of the new security. This means your new basis is higher, which will result in a smaller capital gain (or a larger capital loss) when you eventually sell the new security. While the immediate tax benefit is denied, the loss is not entirely lost; it’s deferred. Understanding this deferral is key to long-term tax planning.

Potential Pitfalls and How to Avoid Them

While tax-loss harvesting 2026 is a powerful tool, it’s not without its complexities. Being aware of common mistakes can help you navigate this strategy successfully.

Ignoring the Wash Sale Rule

As highlighted earlier, this is the most common mistake. Always double-check your transactions for the 61-day window. Many brokerage platforms have systems in place to warn you about potential wash sales, but ultimate responsibility rests with the investor.

Selling for the Sake of Selling

Never let tax considerations dictate your entire investment strategy. The primary goal of investing is to achieve your financial objectives. While harvesting losses can provide tax benefits, selling a good long-term investment just to claim a small loss might not be in your best interest if you believe in its future growth potential. Always consider the investment merits first.

Not Accounting for Transaction Costs

While many brokerages offer commission-free trading, some transactions may still incur fees. These costs can eat into the benefits of harvesting, especially for small losses. Ensure the tax savings outweigh any transaction costs.

Miscalculating Basis

Accurately tracking your cost basis is crucial. If you’ve made multiple purchases of the same security at different prices, you need to use a consistent accounting method (e.g., specific identification, first-in, first-out (FIFO), or average cost for mutual funds). Specific identification often allows for the most precise harvesting, as you can choose which specific lots of shares to sell.

Calculating Your Tax Savings with Tax-Loss Harvesting

Let’s illustrate how tax-loss harvesting 2026 can impact your tax bill.

Scenario 1: Offsetting Capital Gains

Imagine you have realized $10,000 in short-term capital gains from selling a rapidly appreciating stock. You also identify an investment in your portfolio that has a $12,000 unrealized loss. By selling this losing investment, you realize a $12,000 capital loss.

- Your $12,000 capital loss first offsets your $10,000 short-term capital gain, reducing your net capital gain to $0.

- You now have an excess capital loss of $2,000 ($12,000 – $10,000).

- This $2,000 excess loss can then be used to offset $2,000 of your ordinary income.

If you are in the 24% tax bracket, offsetting $10,000 in short-term gains (taxed at ordinary income rates) saves you $2,400. Plus, offsetting $2,000 of ordinary income saves you an additional $480. Total tax savings: $2,880.

Scenario 2: Offsetting Ordinary Income Only

Suppose you have no capital gains for the year, but you have an investment with a $5,000 unrealized loss. You decide to sell it to realize the loss.

- You have a net capital loss of $5,000.

- You can use $3,000 of this loss to offset your ordinary income for the current year.

- The remaining $2,000 in capital losses ($5,000 – $3,000) can be carried forward to future tax years.

If you are in the 24% tax bracket, deducting $3,000 from your ordinary income saves you $720 in taxes for the current year. The $2,000 carried forward can be used in subsequent years to offset future capital gains or another $3,000 of ordinary income.

These examples highlight the significant benefits of proactively applying tax-loss harvesting 2026 to your financial planning.

Integrating Tax-Loss Harvesting into Your Long-Term Financial Plan

Tax-loss harvesting should not be viewed as a one-time event but rather as an ongoing component of a robust financial strategy. By regularly reviewing your portfolio and identifying opportunities, you can consistently reduce your tax liability over time.

Regular Portfolio Reviews

Make it a habit to review your investment portfolio at least quarterly, but especially towards the end of the year. This allows you to identify any underperforming assets that could be candidates for harvesting. Market downturns, even temporary ones, present prime opportunities.

Working with a Financial Advisor

A qualified financial advisor can be an invaluable resource for implementing tax-loss harvesting 2026. They can help you:

- Identify appropriate investments to sell for a loss.

- Ensure compliance with the wash sale rule.

- Integrate harvesting with your overall financial goals, risk tolerance, and asset allocation strategy.

- Accurately track your cost basis and apply losses correctly on your tax returns.

- Stay informed about changes in tax laws that might affect your strategy.

Automation Tools

Many modern investment platforms and robo-advisors offer automated tax-loss harvesting services. These tools continuously monitor your portfolio and automatically execute trades to harvest losses when opportunities arise, while also managing the wash sale rule by purchasing similar, non-identical securities. This can be particularly useful for investors with diversified portfolios who prefer a hands-off approach.

Conclusion: Harnessing the Power of Tax-Loss Harvesting 2026

Tax-loss harvesting 2026 is a sophisticated yet accessible strategy that every investor should consider. By strategically realizing capital losses, you can significantly reduce your tax burden, offset capital gains, and even lower your ordinary income by up to $3,000 annually. The key to success lies in understanding the rules, especially the wash sale rule, maintaining diligent records, and integrating this practice into your broader financial planning.

As you plan for the tax year 2026, take the time to review your investment portfolio, identify potential losses, and develop a harvesting strategy. Whether you manage your investments independently or work with a financial professional, proactive tax planning can lead to substantial savings and help you achieve your long-term financial goals. Don’t leave money on the table; make tax-loss harvesting a cornerstone of your investment approach.

Contributions 2026: Strategies for Retirement Savings")