Federal Reserve Rate Hikes: Mortgage & Loan Impact in 3 Months

Unpacking the Federal Reserve’s Latest Interest Rate Hikes: What They Mean for Your Mortgage and Loans in the Next 3 Months

The financial landscape is constantly shifting, and few entities wield as much influence over its contours as the Federal Reserve. When the Fed moves, the entire economy feels the ripple effect. Recently, the Federal Reserve has continued its aggressive stance on interest rate hikes, a move designed to combat persistent inflation. But what do these Fed rate hikes truly mean for the average American household, particularly concerning their mortgages and other loans, not just now, but specifically over the next three months?

Understanding the implications of these monetary policy shifts is not merely an academic exercise; it’s a critical component of sound personal financial planning. From the monthly payments on your home loan to the interest accrued on your credit cards and personal loans, the Fed’s decisions can have a tangible and immediate impact on your wallet. This comprehensive guide will delve into the mechanics of these rate increases, analyze their expected effects on various types of loans, and provide actionable advice to help you navigate the evolving financial environment in the short term.

We’ll break down the jargon, provide clear explanations, and offer insights into what you can expect in the coming 90 days. Whether you’re a homeowner, a prospective buyer, or someone managing existing debt, this article aims to equip you with the knowledge needed to make informed decisions and safeguard your financial well-being.

The Federal Reserve and Its Mandate: Why the Fed Rate Hikes?

To grasp the significance of the recent Fed rate hikes, it’s essential to understand the Federal Reserve’s dual mandate: to achieve maximum employment and maintain price stability. In recent times, the latter has taken center stage. Inflation, characterized by a sustained increase in the general price level of goods and services, has soared to levels not seen in decades, eroding purchasing power and creating economic uncertainty.

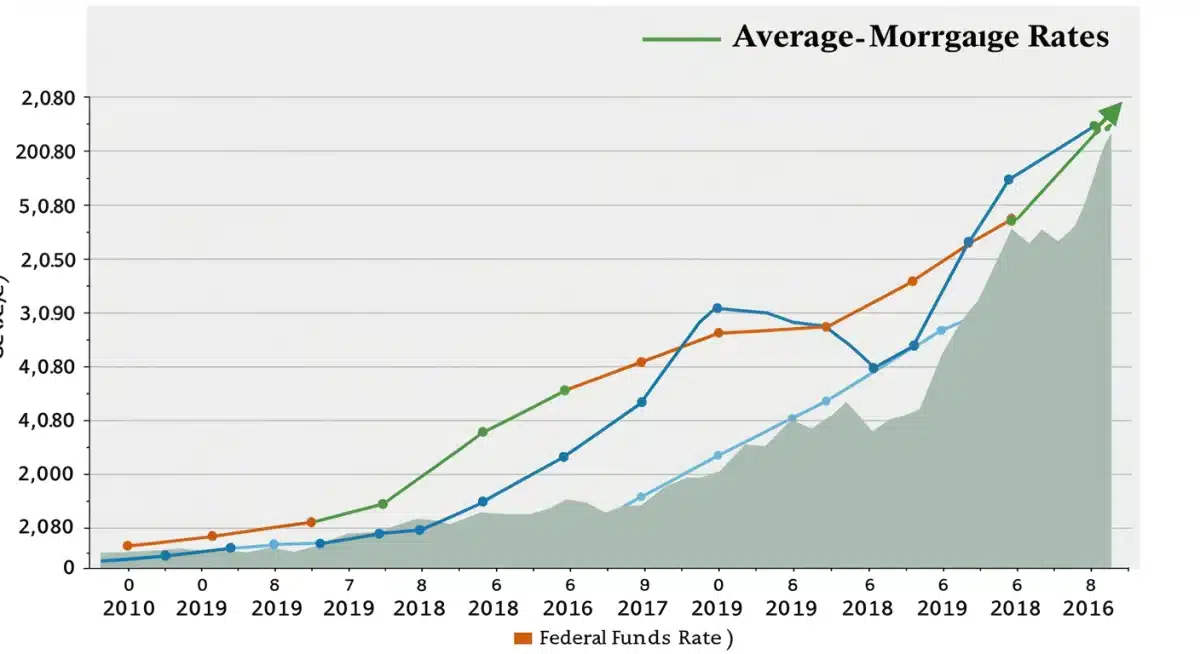

The primary tool the Fed uses to influence the economy and control inflation is the federal funds rate. This is the target interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. While it’s not the rate consumers directly pay, changes to the federal funds rate have a cascading effect throughout the financial system, influencing everything from prime rates to mortgage rates and savings account yields.

When the Fed raises the federal funds rate, it makes borrowing more expensive for banks. These higher costs are then passed on to consumers and businesses in the form of higher interest rates on loans. The intention behind these Fed rate hikes is to cool down an overheating economy by discouraging borrowing and spending, thereby reducing demand and, consequently, inflationary pressures. Conversely, lowering rates is meant to stimulate economic activity.

The recent series of Fed rate hikes reflects the central bank’s determination to bring inflation back down to its target of 2%. While these actions are necessary for long-term economic health, they inevitably create short-term challenges for borrowers and can impact investment strategies. The speed and magnitude of these increases have been particularly noteworthy, signaling a strong commitment from the Fed to address inflation head-on.

Understanding this fundamental mechanism is crucial for interpreting the forthcoming effects on your financial obligations. The Fed’s actions are not arbitrary; they are calculated responses to economic data, aiming to steer the economy toward a more stable and sustainable path, even if the journey involves some turbulence for borrowers.

How Fed Rate Hikes Directly Impact Mortgages

For most homeowners, their mortgage is their largest financial commitment. Therefore, changes in interest rates are often met with a mix of anxiety and careful consideration. It’s important to distinguish between fixed-rate and adjustable-rate mortgages (ARMs) when discussing the impact of Fed rate hikes.

Fixed-Rate Mortgages (FRMs)

If you have a fixed-rate mortgage, the good news is that your interest rate and monthly payments are locked in for the life of the loan. This means that recent or future Fed rate hikes will not directly affect your current mortgage payments. Your stability is one of the primary benefits of choosing a fixed-rate product. However, if you are considering refinancing your fixed-rate mortgage, the landscape has changed significantly. Refinancing now means securing a new loan at current, higher interest rates, which would likely result in higher monthly payments unless you significantly shorten the loan term or borrow less.

For prospective homebuyers, the scenario is different. New fixed-rate mortgages are now being issued at substantially higher rates than a year or two ago. This directly translates to higher monthly payments for the same loan amount, reducing purchasing power and making homeownership less affordable. Over the next three months, if the Fed continues its trajectory of Fed rate hikes, we can expect fixed mortgage rates to either remain elevated or climb even further, albeit perhaps at a slower pace as the market has already priced in many anticipated increases.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages are where the immediate and most direct impact of Fed rate hikes will be felt. ARMs typically have an initial fixed-rate period (e.g., 3, 5, 7, or 10 years), after which the interest rate adjusts periodically based on a predetermined index, often tied to the Secured Overnight Financing Rate (SOFR) or the Constant Maturity Treasury (CMT) rates. These indices are highly sensitive to the federal funds rate.

If your ARM is nearing the end of its fixed-rate period, or if it has already begun to adjust, you are likely to see your interest rate increase significantly in the coming three months. This will lead to higher monthly mortgage payments. The extent of the increase will depend on the terms of your specific ARM, including its adjustment cap (the maximum amount the rate can increase in a given period) and its lifetime cap. Borrowers with ARMs should proactively review their loan documents to understand their adjustment schedule and potential payment changes.

Refinancing and Home Equity Loans

The environment for refinancing has become less attractive for most homeowners with existing fixed-rate mortgages. As mentioned, new rates are higher. However, for those with ARMs facing significant payment increases, refinancing into a fixed-rate mortgage might still be a viable strategy to lock in a rate, even if it’s higher than their initial ARM rate, to gain payment stability. This decision requires careful calculation of closing costs versus long-term savings or stability.

Home equity lines of credit (HELOCs) and home equity loans (HELs) are also directly affected by Fed rate hikes. HELOCs, in particular, often have variable interest rates tied to the prime rate, which moves in lockstep with the federal funds rate. If you have a HELOC, expect your minimum payments to increase as interest rates rise. Home equity loans, while often fixed-rate, will be issued at higher rates for new borrowers, making them more expensive to acquire.

The Ripple Effect: Fed Rate Hikes on Other Loans and Debt

The influence of Fed rate hikes extends far beyond mortgages. Virtually all forms of credit are impacted, though the speed and magnitude of the effect can vary. Understanding these broader implications is vital for managing your overall debt portfolio.

Credit Cards

Credit card interest rates are almost universally variable and are typically tied to the prime rate. When the Federal Reserve raises the federal funds rate, the prime rate follows suit almost immediately. This means that if you carry a balance on your credit cards, your annual percentage rate (APR) will increase, leading to higher interest charges and larger minimum payments. This effect is usually felt within one or two billing cycles following a Fed rate hike.

Over the next three months, if the Fed continues its tightening policy, credit card debt will become even more expensive. This underscores the importance of paying down high-interest credit card balances as quickly as possible. Strategies like balance transfers to cards with promotional 0% APR periods can offer temporary relief, but it’s crucial to pay off the transferred balance before the promotional period ends and the higher rate kicks in.

Auto Loans

The impact of Fed rate hikes on auto loans is generally more pronounced for new loans rather than existing ones. Most auto loans are fixed-rate, meaning your interest rate and monthly payment remain constant once the loan is originated. However, for those looking to purchase a new or used vehicle in the coming months, expect to encounter higher interest rates than those available a year ago. This increases the total cost of the vehicle and can make monthly payments less affordable, potentially pushing buyers toward longer loan terms or less expensive vehicles.

While existing auto loans are largely insulated, the overall cost of new car financing will continue to reflect the Fed’s policy. This could dampen demand in the automotive sector, as consumers grapple with higher borrowing costs on top of already elevated vehicle prices.

Personal Loans

Personal loans, which can be secured or unsecured, also feel the squeeze from Fed rate hikes. Similar to auto loans, if you have an existing fixed-rate personal loan, your payments will not change. However, new personal loans will be offered at higher interest rates. Variable-rate personal loans will see their rates adjust upwards, leading to increased monthly payments.

Many consumers use personal loans for debt consolidation or unexpected expenses. In an environment of rising rates, the cost-effectiveness of using a personal loan for consolidation needs careful evaluation. While it can still be a good option for simplifying payments, the interest rate may be less favorable than it would have been previously.

Student Loans

The vast majority of federal student loans are fixed-rate, meaning current borrowers are largely unaffected by Fed rate hikes. For new federal student loans, the interest rates are set annually by Congress and are not directly tied to the federal funds rate in the same immediate way as other consumer loans, though broader economic conditions influenced by the Fed can play a role in their determination. However, private student loans often have variable interest rates tied to market indices, which will increase with Fed rate hikes. Borrowers with variable-rate private student loans should anticipate higher payments in the coming months. Consolidating or refinancing these into a fixed-rate loan could be a consideration, but again, current rates will be higher than in the recent past.

Economic Outlook and Future Fed Actions: What to Expect in the Next 3 Months

Predicting the Federal Reserve’s exact moves is challenging, as their decisions are data-dependent and subject to change. However, based on current economic indicators and the Fed’s stated objectives, we can form reasonable expectations for the next three months regarding Fed rate hikes and their subsequent economic impact.

Inflationary Pressures

The primary driver behind the recent Fed rate hikes is inflation. While there have been some signs of inflation moderating, it remains stubbornly high, particularly in core services. The Fed will be closely watching key inflation metrics, such as the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index. If inflation remains elevated, the likelihood of further, albeit potentially smaller, rate hikes within the next three months increases.

Conversely, a significant and sustained decline in inflation could lead the Fed to pause its tightening cycle. However, the Fed has signaled a strong commitment to bringing inflation down to its 2% target, suggesting they are prepared to continue raising rates until there is clear evidence of disinflation.

Labor Market Strength

The labor market has remained remarkably robust despite the aggressive monetary tightening. Low unemployment rates and strong wage growth are positive for workers but can also contribute to inflationary pressures. The Fed will be monitoring job growth, wage inflation, and unemployment figures. A cooling labor market, with some increase in unemployment, might give the Fed more room to ease off on Fed rate hikes. However, a persistently tight labor market could necessitate further action.

Economic Growth

Higher interest rates are designed to slow down economic activity. The risk of a recession is a significant concern, and the Fed is attempting a ‘soft landing’ – bringing down inflation without triggering a severe economic downturn. GDP growth figures, consumer spending, and business investment will be key indicators. If the economy shows signs of significant contraction, the Fed might become more cautious with future Fed rate hikes. However, their current focus is clearly on inflation control, even if it means some economic pain.

Market Expectations

Financial markets typically react quickly to Fed announcements and economic data, often pricing in anticipated rate changes well in advance. Over the next three months, market expectations for future Fed rate hikes will continue to be a significant factor influencing bond yields and, consequently, mortgage rates. Volatility can be expected as new data is released and Fed officials make public statements. It’s safe to assume that interest rates will remain elevated, with the possibility of further modest increases, rather than significant decreases, in the short term.

Strategies for Navigating the Rising Rate Environment

Given the persistent impact of Fed rate hikes, proactive financial planning is more important than ever. Here are some strategies to consider over the next three months and beyond:

Review and Re-evaluate Your Budget

The first step is to get a clear picture of your current financial situation. Review your income and expenses meticulously. Identify areas where you can cut back, especially if your variable loan payments are increasing. Create a detailed budget that accounts for potential higher interest costs on credit cards, ARMs, or HELOCs. Understanding your cash flow is paramount to avoiding financial strain.

Prioritize High-Interest Debt

With Fed rate hikes making borrowing more expensive, aggressively paying down high-interest debt, such as credit card balances and variable-rate personal loans, should be a top priority. Consider the ‘debt avalanche’ method (paying off the debt with the highest interest rate first) to minimize the total interest paid over time. Even small extra payments can make a significant difference.

Consider Refinancing for ARMs (Carefully)

If you have an adjustable-rate mortgage and your fixed-rate period is ending soon, or if you’re already seeing significant payment increases, explore refinancing into a fixed-rate mortgage. While current fixed rates are higher than historical lows, locking in a predictable payment can provide peace of mind and protection against further Fed rate hikes. Compare offers from multiple lenders and factor in closing costs to determine if it’s a financially sound move for your specific situation.

Explore Loan Consolidation

For individuals with multiple high-interest debts, consolidating them into a single loan could simplify management and potentially lower your overall interest burden, especially if you can secure a fixed-rate personal loan or balance transfer card with a lower rate than your existing debts. However, be wary of extending the loan term significantly, which could lead to paying more interest over the long run.

Build or Bolster Your Emergency Fund

Economic uncertainty and rising costs make an emergency fund more critical than ever. Aim to have at least three to six months’ worth of essential living expenses saved in an easily accessible account. This fund can provide a buffer against unexpected expenses or income disruptions, reducing the need to take on new, more expensive debt.

Delay Non-Essential Large Purchases

If you were planning a major purchase that requires financing, such as a new car or a significant home renovation, consider delaying it if possible. Higher interest rates mean these purchases will be more expensive. Waiting might allow you to save more for a larger down payment, reducing the amount you need to borrow, or potentially benefit from lower rates if economic conditions shift in the future.

Consult a Financial Advisor

For complex financial situations or if you feel overwhelmed by the changes, consider consulting a qualified financial advisor. They can provide personalized advice tailored to your specific circumstances, helping you develop a robust strategy to navigate the current economic climate and the impact of Fed rate hikes.

Conclusion: Adapting to the New Normal of Fed Rate Hikes

The Federal Reserve’s ongoing commitment to curbing inflation through Fed rate hikes has ushered in a new era for borrowers and the broader economy. Over the next three months, we can expect to see continued pressure on mortgage rates, particularly for adjustable-rate products, and increased costs for credit card debt and new loans. While the immediate outlook suggests elevated borrowing costs, these measures are ultimately aimed at restoring economic stability.

For individuals, the key to navigating this environment lies in proactive engagement with personal finances. By understanding how these Fed rate hikes translate to your specific loans, diligently managing your budget, prioritizing high-interest debt, and exploring strategic refinancing options where appropriate, you can mitigate the negative impacts and even find opportunities for financial optimization. Staying informed about economic developments and the Fed’s future signals will also be crucial in making timely and effective financial decisions. The financial landscape is dynamic, but with careful planning and informed action, you can successfully adapt to these changes.

Federal Reserve Rate Hikes: Key Takeaways

- Purpose: The Fed raises rates to combat inflation by making borrowing more expensive, thus slowing economic activity.

- Mortgages: Fixed-rate mortgages are unaffected; adjustable-rate mortgages (ARMs) will see payments rise as their rates adjust. New fixed-rate mortgages are more expensive.

- Other Loans: Credit card APRs will increase immediately. New auto and personal loans will carry higher interest rates. Variable-rate private student loans will also become more costly.

- Next 3 Months: Expect continued elevated interest rates, with potential for further small increases, depending on inflation and labor market data.

- Actionable Advice: Prioritize paying down high-interest debt, review your budget, consider ARM refinancing, and build an emergency fund.